Housing Affordability in Oregon

April 04, 2025Housing affordability has been a hot topic as of late due to a substantial increase in housing prices in Oregon and across the U.S. since 2020. Listing prices for houses in Oregon increased over $140,000 (34%) from 2019 to 2023.

Fundamentally, the price of housing is a function of housing supply and housing demand. Housing supply is negatively correlated with price. That is, the more housing supply the lower the price, and vice versa. Housing demand is positively correlated with price. In other words, the more demand for housing the higher the price, and vice versa. Another factor that has changed the affordability picture in recent years is higher mortgage interest rates than prior to the pandemic, significantly reducing the home price that is affordable for the typical household.

Housing Demand Outstripping Supply

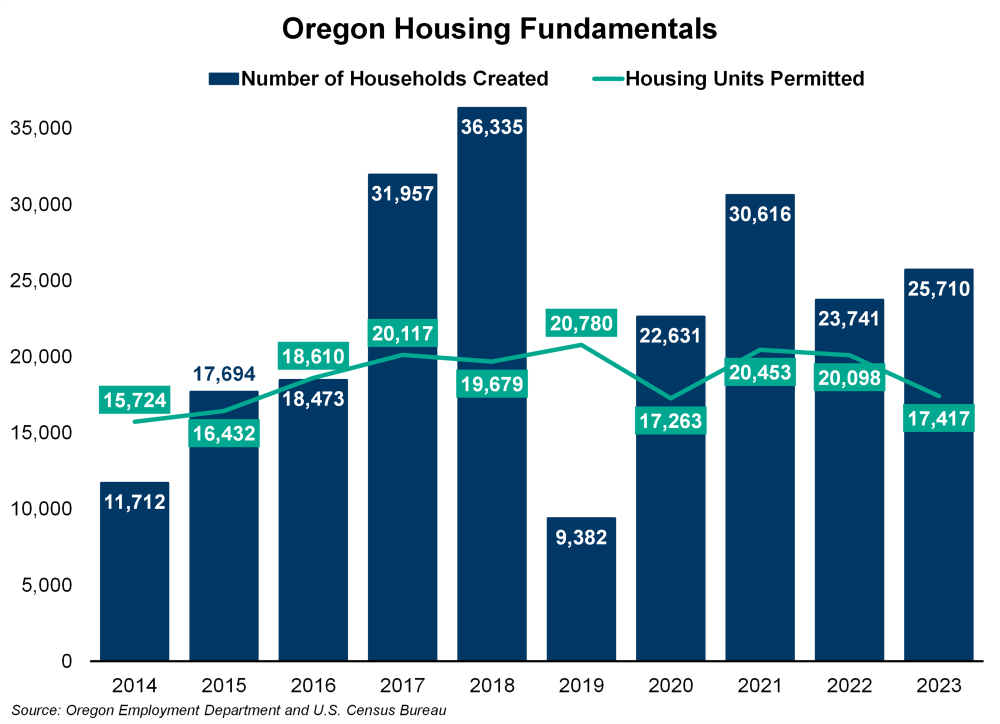

There are a couple ways to track housing supply. One measure is the change in housing permits, or the number of residential housing units approved for construction each year, which is tracked by the U.S. Census Bureau through its Building Permits Survey.

On the housing demand side, we can look at the annual change in the number of households. The Census tracks the number of households in a given geography through the decennial census and the American Community Survey. According to the Census, “a household is composed of one or more people who occupy a housing unit.” Households can usually form by people moving into the state or by people moving out of a co-habitation situation – for example, children moving out of their parents’ house.

Comparing the trends of building permits approval and household formation allows us to see the relationship between housing supply and demand.

In Oregon, growth in the number of households outpaced the number of new units approved for building in six of the last seven years, going back to 2017. Housing demand has outpaced housing supply to the point where there is only a 0.8% housing vacancy rate in Oregon, a full percentage point below the vacancy rate a decade ago, according to the U.S. Census Bureau.

In the 2010s, Oregon’s increase in household formation was largely due to strong in-migration. Though in-migration to Oregon has somewhat stagnated since 2020, one big trend to come out of the COVID-19 pandemic in 2020 was a significant increase in the household formation rate. In normal terms, this means that people moved out of shared households and formed their own, such as kids moving out of their parent’s home or roommates moving out of shared living spaces.

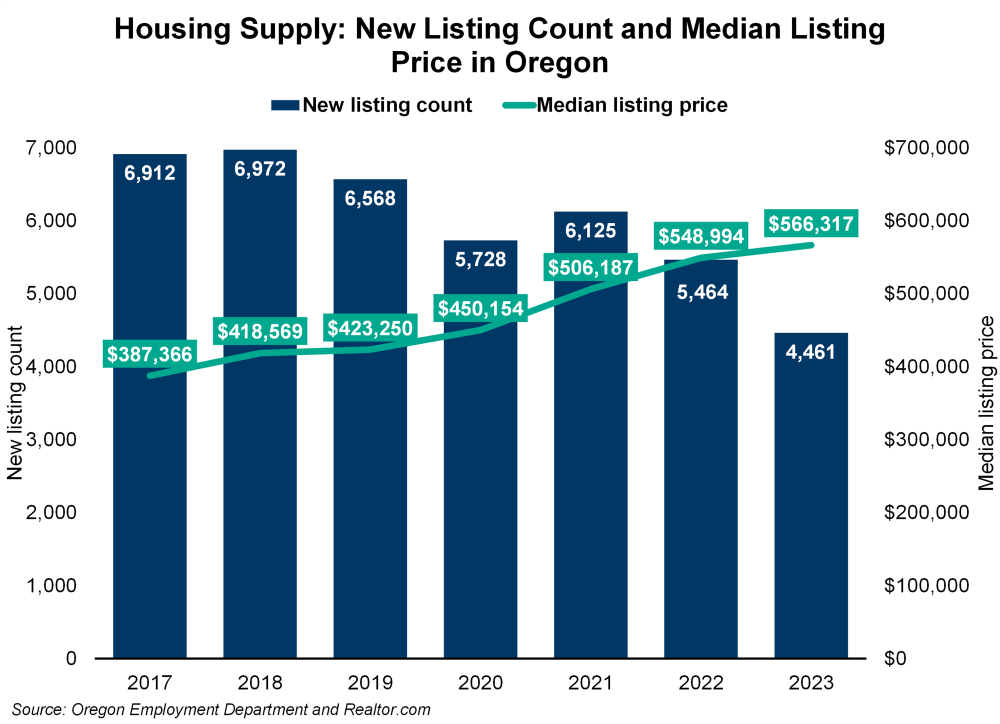

The supply of available homes for sale plummeted in 2023. Looking specifically at how the limited supply of housing affects prices, we can look at housing listing data from Realtor.com, which tracks the number of new listings of houses for purchase in Oregon and median price for those listings.

The number of new listings in Oregon hovered above 6,500 from 2017 to 2019. It then dropped below 6,000 new listings in 2020 and then plummeted to around 4,500 new listings in 2023. From 2019 to 2023, the number of new listings in Oregon dropped 32%. Correspondingly, the median listing price increased 34% from 2019 to 2023.

Mortgage Rates Are Higher than in Recent History

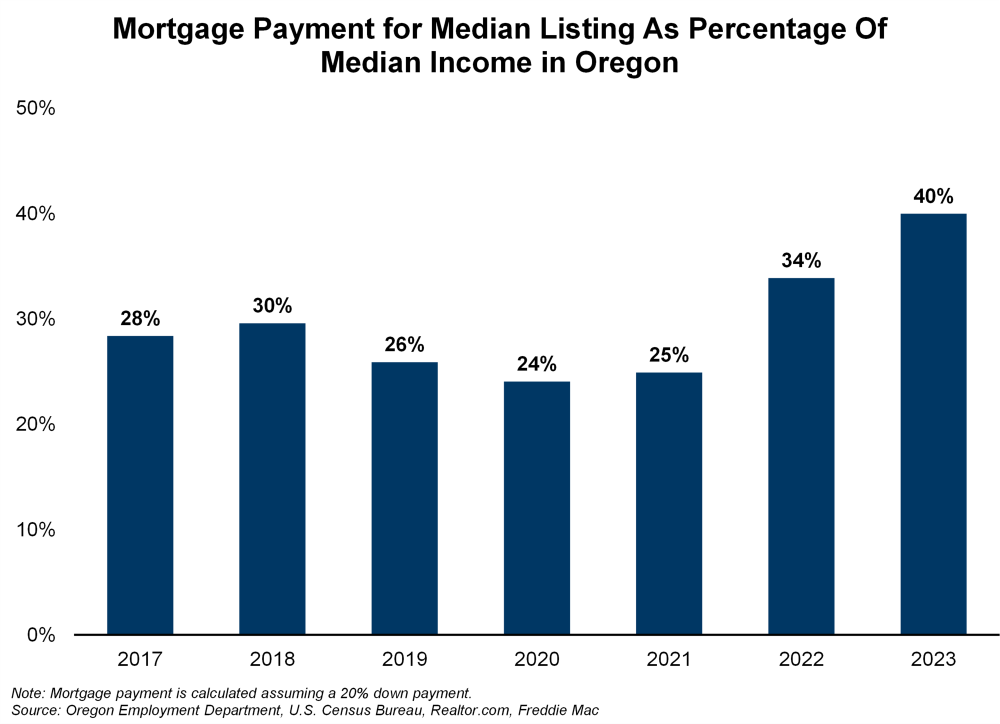

Home prices are not the only factor in affordability for the typical household. For prospective home buyers who will take out a mortgage, the interest rate on the mortgage also affects the price of housing. The higher the mortgage rate, the higher the monthly payment.

The graph shows an estimated monthly mortgage payment as a percentage of the median monthly household income in Oregon. The monthly mortgage payment is estimated assuming a fairly generous 20% down payment, using the median listing price for a home according to Realtor.com and using the average interest rate for a mortgage according to Freddie Mac.

Comparing the estimated mortgage payment to the median monthly household income, we see that the share spiked in 2023. This is in part due to the median housing price growth outpacing the growth in the median household income. From 2017 to 2023, the median listing price increased 46%, and the median household income increased 42%. The other major reason mortgage payments increased is a spike in mortgage rates, which increased from an average of 3.0% in 2021, to 5.3% in 2022, to 6.8% in 2023. Mortgage rates are determined by many factors, including inflation, consumer spending, the Federal Reserve’s monetary policy, the bond market, and the housing market. In 2022 and 2023, high inflation and increases in the federal funds rate contributed to the high mortgage rate.

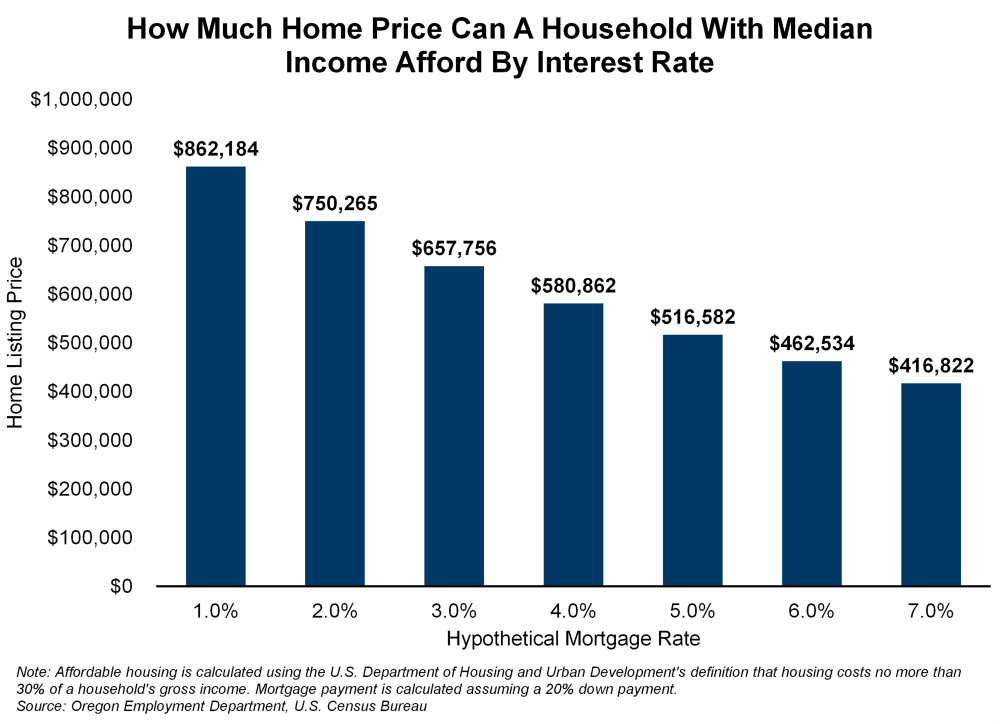

Mortgage rates make a big difference in the home price a person can afford. For the 2023 median home listing price, a one percentage-point difference in the mortgage rate changes the monthly mortgage payment between $200 to $300. Over the duration of a mortgage, that can make a difference in the home price a person can afford upwards of $45,000 per percentage point.

Mortgage rates are likely to remain higher than before the pandemic for some time. While inflation has moderated, consumer prices are still increasing faster than prior to the pandemic and remain above the Federal Reserve’s target, leaving little justification for reducing borrowing rates quickly.

More Housing Units Are Needed to Address the Current Shortage

Housing prices have skyrocketed recently and the effects are felt by all across all of Oregon. Matching housing supply to demand requires continuing public and private focus and investment. The Oregon Housing and Community Services department covers housing in more depth in their 2024 State of the State’s Housing Report.

You can read about details of the apartment market in the article Housing Affordability: The Rental Market in Oregon.

To learn more about demographics of renting and owning in Oregon, visit the article Characteristics of Home Ownership and Renting in Oregon.